Bajaj Housing Finance is bankable, but not a bank

Earlier this month, Bajaj Housing Finance filed a draft offer document with the capital market regulator to offer shares worth about ₹7,000 crore to the public for the first time. Of this, ₹3,000 crore of shares are being sold by parent Bajaj Finance. The remaining ₹4,000 crore will come in from new shares, which will help it expand its housing-finance business. While Bajaj Housing is an efficient and profitable player in home loans, it faces structural issues, the most important being competition from banks, which have a natural advantage.

Bajaj Housing is India’s second-largest housing finance company (HFC) as of 2023-24 with assets of ₹91,370 crore. LIC Housing Finance is the leader, with ₹2.87 trillion in assets. HDFC previously held the top stop before it merged with HDFC Bank in July 2023.

Banks have an advantage over non-bank financiers as they can raise funds at a lower rate of interest through savings and current deposits. HFCs, on the other hand, have to borrow from banks or raise funds via bonds. In late-2022, CRISIL wrote, “HFCs are expected to continue losing home-loan market share to banks amid stiff competition.”

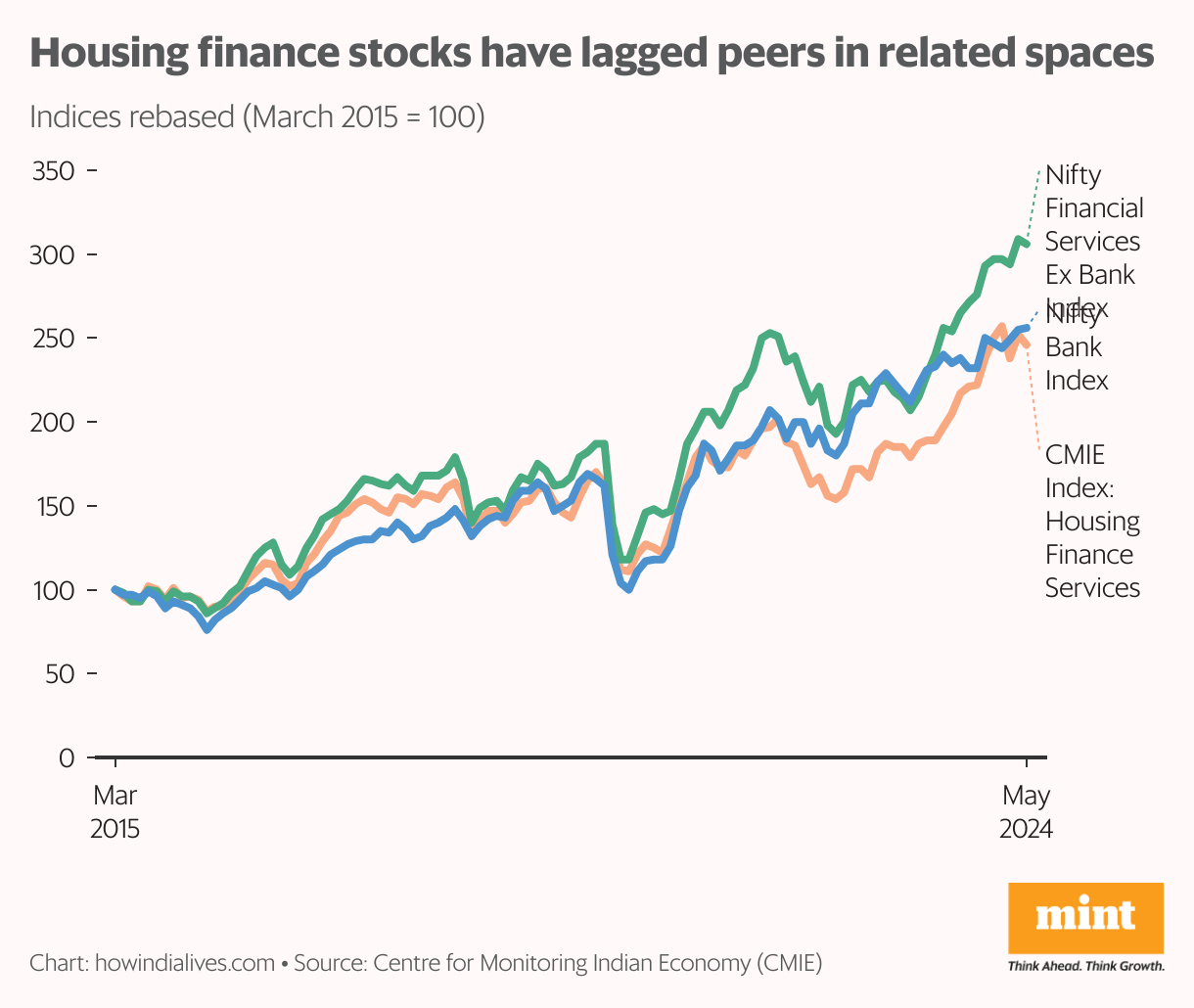

As a result, stocks of HFCs have lagged those of banks and fellow non-banking finance companies (NBFCs) that operate in areas – such as gold loans and auto loans – that have higher margins.

Also Read: Indian IPO market poised for strong growth as dust settles on election results

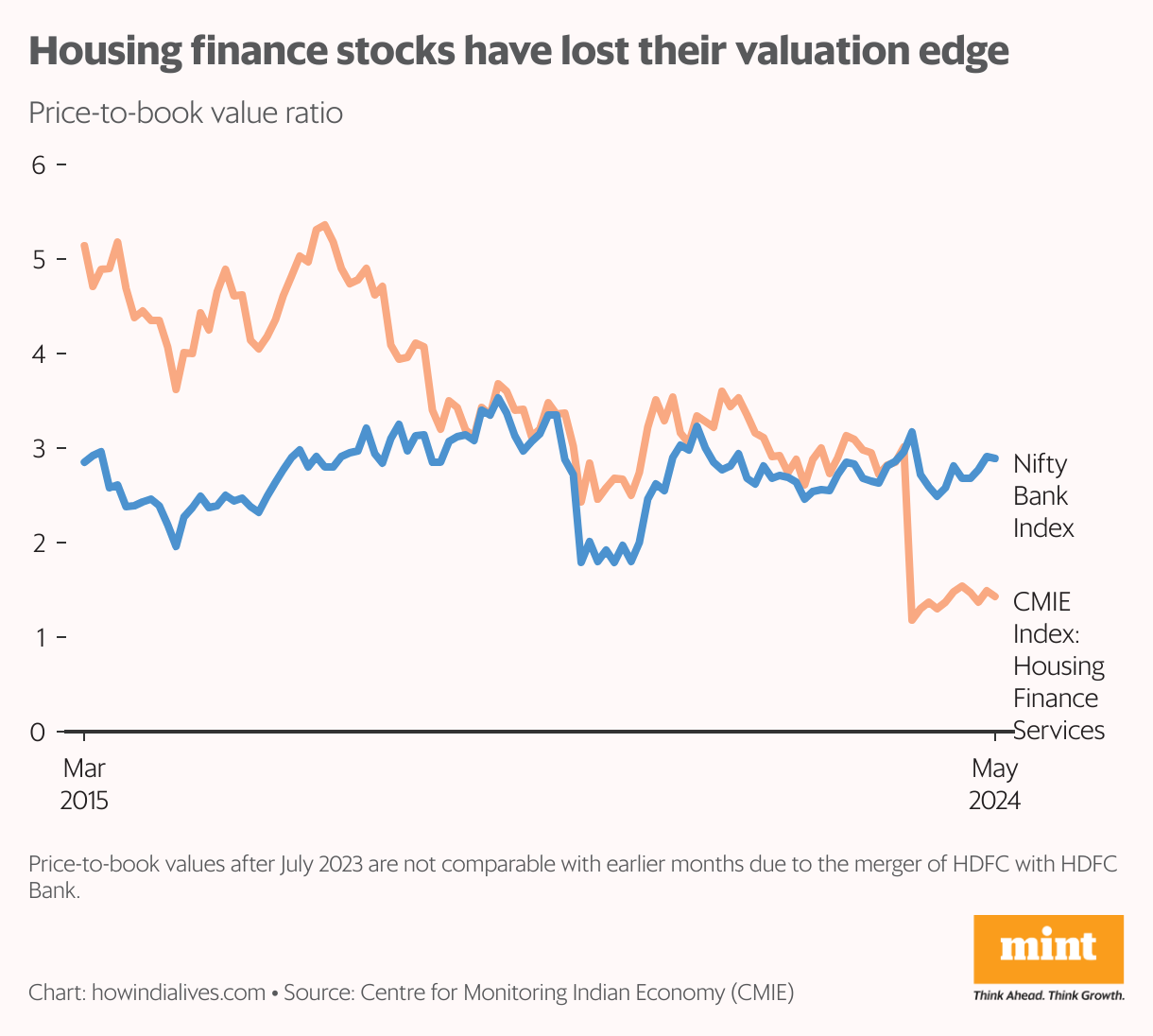

Interestingly, until a few years ago, HFCs traded at higher valuations than banks in terms of the price-to-book value. But the NBFC crisis in 2018, triggered by the collapse of IL&FS, led to a re-rating of such stocks.

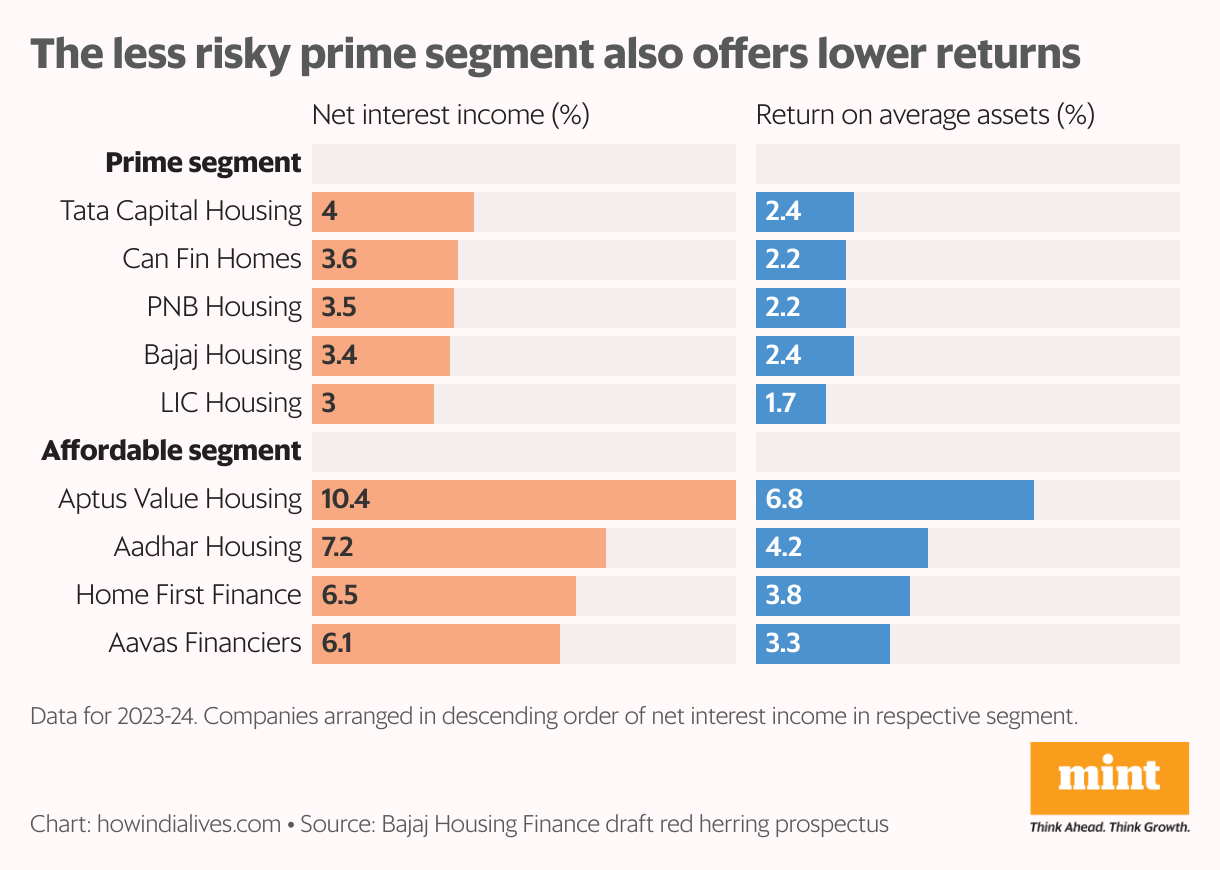

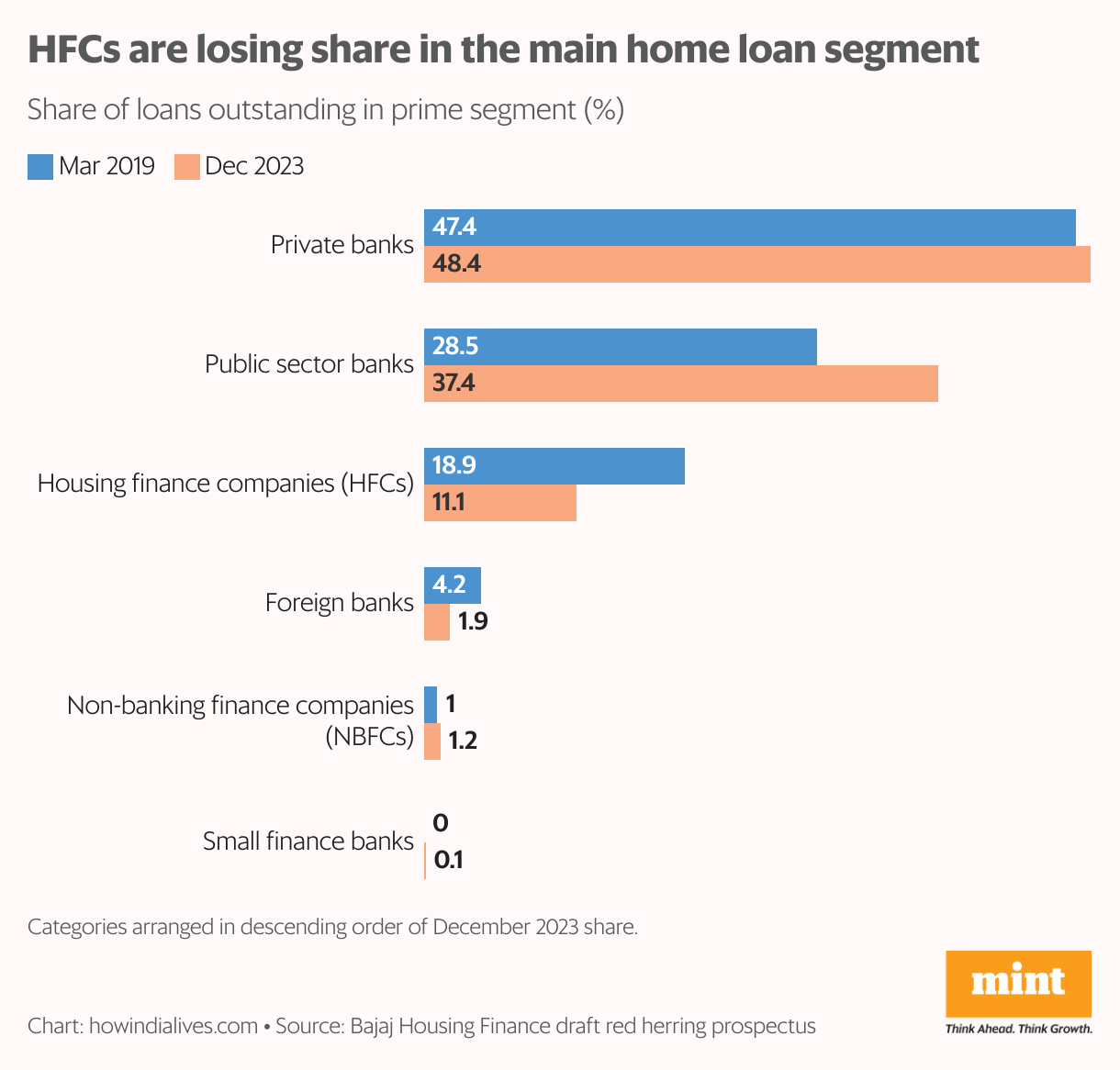

Prime vs affordable segment

Bajaj Housing primarily operates in the so-called ‘prime’ segment of the market, where the ticket size of a loan is above ₹50 lakh. In contrast, Aadhar Housing, which went public in May, operates in the affordable segment (ticket size below ₹25 lakh). Besides the loan size, the difference between the two segments is in the type of borrowers and the risks they pose.

Prime segment loans are perceived as safer, as a greater share of their borrowers are salaried. To compensate for their increased risk, interest rates in the affordable segment tend to be higher. This is reflected in the net interest income and return on average assets of affordable segment lenders. “One segment where HFCs have been growing relatively faster is affordable housing loans, where competition from banks is limited,” said CRISIL in its 2022 report. “Given their relatively smaller footprint and large underlying demand, AHFCs are expected to keep growing faster than traditional HFCs.”

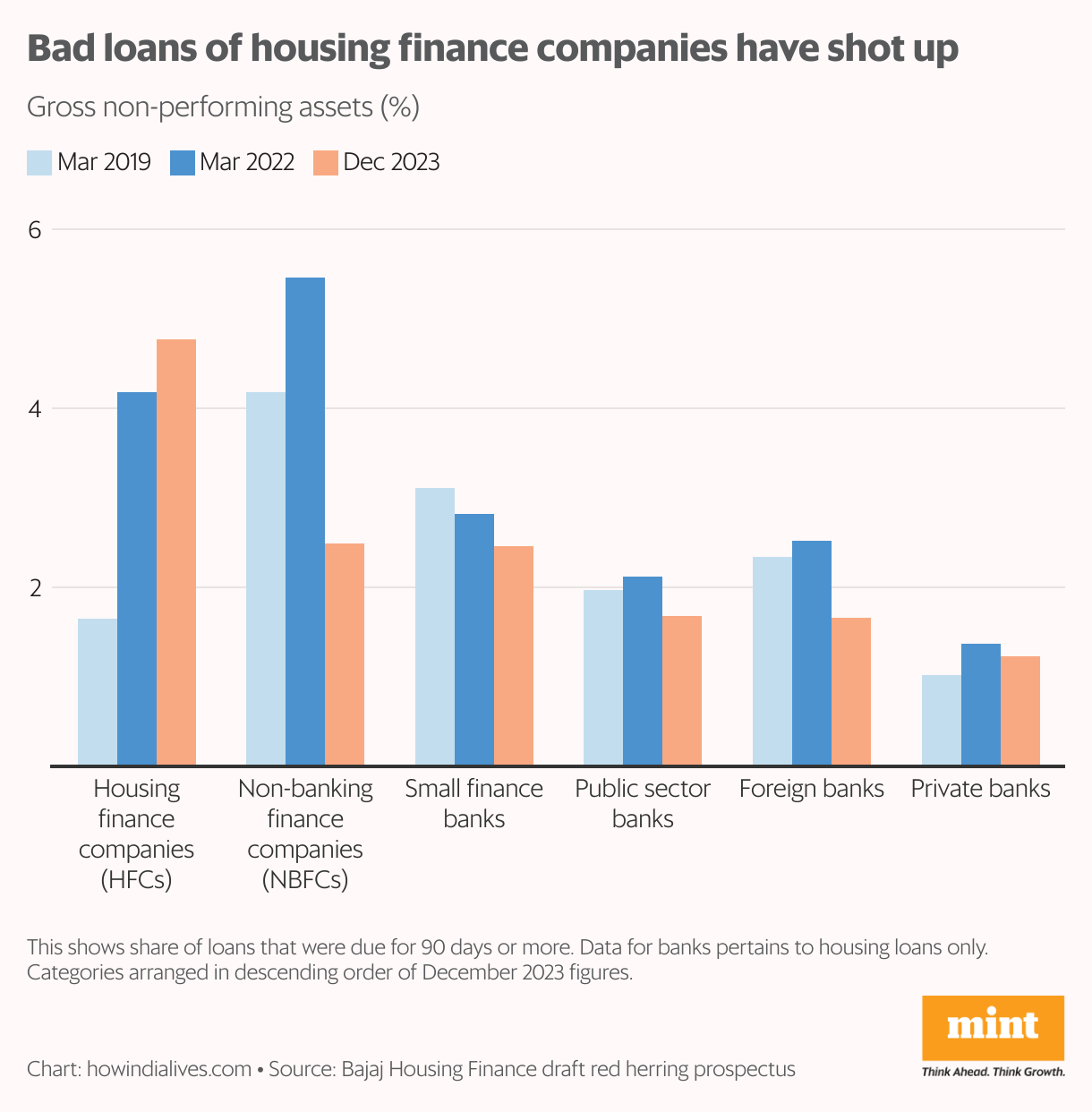

Quality of loans

As a whole, though, HFCs have seen more loans turn bad than various types of banks. The share of loans in HFC portfolios that have not been serviced for 90 days or more rose from 1.65% in March 2019 to 4.77% in December 2023. This was partly because HFCs target borrowers in the affordable housing segment, which tends to be riskier. As of December 2023, HFCs accounted for about one-third of loans in this segment, as compared to 11% in the prime segment, where banks dominate.

Bajaj Housing Finance, though, is a relatively good performer. As of December 2023, its gross non-performing assets (NPAs) stood at 0.22% of its loans outstanding, against 4.4% for LIC Housing Finance and 3.8% for PNB Housing Finance. According to its issue prospectus, the company focuses on “mass affluent clients”, with an average age of 35-40 years and an average annual salary of above ₹13 lakh. About 88% of its customers are salaried.

Stiff competition

Despite its superior loan quality, Bajaj Housing’s focus on the prime segment is, ironically, also a challenge. This is also the focus of public-sector banks, which have a lower cost of funds. As a result, the market share of HFCs in this segment has decreased steadily from 19% in FY19 to 11% in the first nine months of FY24.

According to CRISIL, “The ability of HFCs to compete with banks in the traditional salaried-home-loan segment remains a challenge given their relatively higher funding costs. And in the non-home loan segments (developer financing and LAP [loans against property]), which have been yield kickers, HFCs’ exposure has reduced in the past few years, which has put pressure on overall spreads.” In the absence of a banking connect, like HDFC, how Bajaj Finance squares up against banks will be a crucial determinant of growth.

www.howindialives.com is a database and search engine for public data.

link

– Advertising, Marketing & Branding")